Client Profile

- Married couple, age 65

- Retirement income needs fully covered by Social Security

- $1,000,000 saved in pre-tax IRA funds

- Goal: Determine whether a Roth IRA conversion would improve lifetime income and legacy outcomes

- Married couple, age 65

- Retirement income needs fully covered by Social Security

- $1,000,000 saved in pre-tax IRA funds

- Goal: Determine whether a Roth IRA conversion would improve lifetime income and legacy outcomes

- Required Minimum Distributions (RMDs) starting at age 73 could increase taxable income and reduce tax efficiency.

- Uncertainty about whether converting to Roth now would provide better after-tax income and inheritance value.

1. Income & Lifestyle Control: Ensured Social Security fully supported living expenses.

2. Tax Planning & Roth Conversion Strategy: Modeled conversion from age 65 to 73 vs. no conversion scenario.

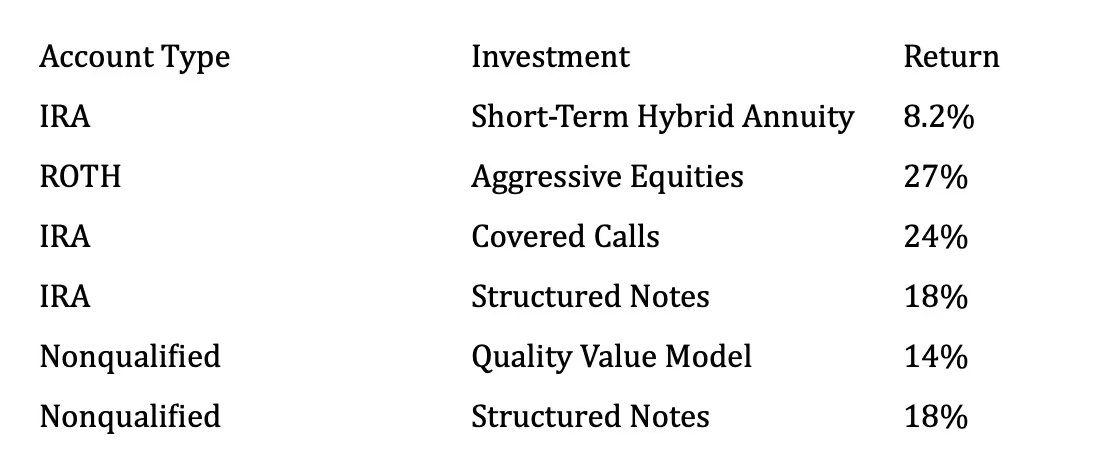

3. Portfolio Design & Investment Strategy: Allocated Roth assets to aggressive growth strategies (27% target return).

4. Legacy & End-of-Life Planning: Compared after-tax inheritance values for heirs under both scenarios.

Conversion increased lifetime income by $224,231 but slightly reduced after-tax inheritance by $482,646.

Old 'Strategy' – Prior to NJM: -20% to +17.5%, averaging 8% over 8 years (inconsistent).

NJM 'All Weather' Approach: +5% to +14%, more consistent performance.